Walk through any new BTR or coliving project in Melbourne right now and you will notice the same thing: high-spec building and room fitouts, concierge services, and rents that put these rooms squarely out of reach for the average renter.

That’s not an accident. It’s a feasibility problem.

The economics of most coliving and BTR developments only stack up at premium price points. High land costs, construction costs, and fitout standards push operators toward the upper end of the market just to make the numbers work. The result? A sector that was supposed to solve affordability is increasingly serving people who don’t actually need the help.

There’s a renter cohort that nobody is building for. Essential workers, graduate professionals, nurses, teachers, tradespeople. People in their mid-twenties to late thirties earning a decent income but completely priced out of renting alone in a well-located suburb. They earn too much to qualify for social housing. They earn too little to justify paying a premium coliving rate. And right now, their only option is an ageing share house with no professional management, no lease certainty, and no design intent whatsoever.

That gap is large, it’s growing, and it’s structurally underserved.

But what if the feasibility argument is also the solution?

At Livko, we’ve been thinking about a format we’re calling Living Clusters, a density-first approach to shared living that makes mid-market rents financially viable without sacrificing quality or liveability.

The concept is straightforward:

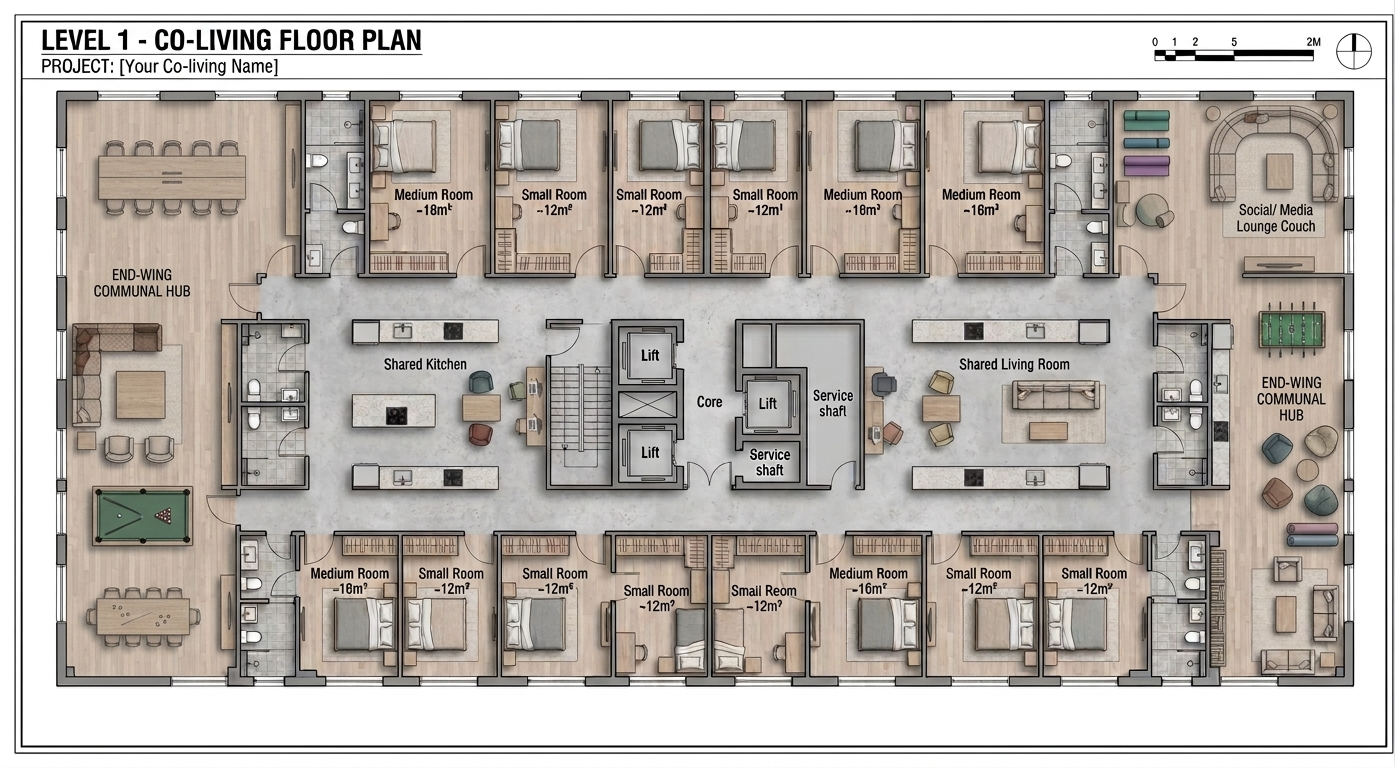

Rather than designing large-format buildings around individual self-contained studios with full kitchens, Living Clusters organise each floor into groups of approximately 9 private rooms, each with their own bathroom, sharing a well-designed communal kitchen and living space. Think less hotel corridor, more a large share house. Purpose-built, professionally managed, and at a scale that makes the numbers work.

This isn’t a new idea internationally. The Mehr als Wohnen cooperative housing project in Zurich a multi-award-winning development including the World Habitat Award has been running exactly this cluster format since 2015. Eleven cluster apartments, each approximately 400 square metres, each housing 9 to 12 residents around a shared kitchen and living space, with private rooms and individual bathrooms. While Zurich’s cooperative housing context differs from Melbourne’s private rental market, the design logic translates directly: clustering private rooms around shared kitchen and living infrastructure produces better density, lower per-room construction cost, and stronger community outcomes than a corridor of self-contained studios. The project has been studied extensively as a model for affordable, high-density urban housing that doesn’t compromise on quality or community.

Melbourne doesn’t have an equivalent. That’s the opportunity.

Why does this change the feasibility?

Individual kitchens carry a construction cost in the range of $15k to $20k per room depending on specification and finish. Across a 45-room building that represents an estimated $675k to $900k in kitchenette construction cost alone.

By shifting to shared kitchens per floor cluster, that cost is consolidated. One well-equipped communal kitchen serving 9 rooms costs an estimated $85k. Across 5 floors that represents a total kitchen investment of approximately $425k, compared to an estimated $675k to $900k for individual kitchenettes across the same 45 rooms. The saving across the building is in the order of $250k to $475k, before accounting for any operational efficiencies or wet area consolidation benefits.

But the more important shift is strategic rather than numerical. Removing fully self-contained units means the development is no longer constrained by the economics of the studio apartment. The focus moves to density and to delivering quality in the areas that actually matter to residents: a well-designed private room, a well-equipped shared kitchen, and a professionally managed building. What was only workable at a premium price point now works at a mid-market one.

A Living Cluster room in an inner-Melbourne suburb at mid-market would target $450 to $480 per week, all-inclusive meaningfully below premium coliving, meaningfully above what a poorly managed share house offers in certainty and quality.

The maths isn’t complicated. The design decision is because it requires choosing density and community over the self-contained studio that the sector has spent the last five years treating as the default.

This isn’t a stripped-back product. It’s a smarter floor plan.

Residents who choose Living Clusters aren’t missing out. Co-working spaces, communal lounges, and shared amenities can all still be part of the building. The difference is purely structural: shared kitchens per floor cluster instead of individual kitchens in every room. That single design decision is what unlocks greater density, recovers meaningful NLA, and makes a genuine mid-market rent point viable, without compromising the living experience that makes coliving worth choosing in the first place.

And the design does something else that operators and investors should pay attention to. Industry data suggests professionally managed coliving sees significantly higher lease renewal rates than conventional rentals a gap that widens further when community is built into the physical layout of the building rather than bolted on as an amenity. The driver isn’t the gym or the co-working space. It’s the community. Social connection built into the physical layout through shared kitchens and cluster living spaces produces retention that self-contained studios structurally cannot replicate. Lower churn means lower vacancy, lower turnover costs, and a more stable income profile for the asset. That’s not a lifestyle argument. That’s an investment thesis.

The premium end of BTR and coliving is crowded. The middle isn’t.

The sector has spent five years proving the concept works at the top of the market. Operators have demonstrated that renters will pay a premium for professionally managed shared living. That proof of concept is valuable. It de-risks the product category. But the premium segment is now competitive, and the yield compression that follows competition is already beginning.

The next opportunity is proving the model works for everyone else and that the numbers can stack without chasing premium rents. That requires a different design approach, a different cost structure, and an operator willing to build for a market that the rest of the sector is largely ignoring.

Living Clusters is Livko’s answer to that question.

Livko is a Melbourne-based shared living operator focused on delivering professionally managed, financially accessible coliving through smart design and operational excellence.

Interested in the Living Clusters concept as a developer, landowner, or capital partner? Let’s talk.

Sources: Mehr als Wohnen, Zurich — Duplex Architekten (2015); Coliving.com Economics Guide (2026) — lease renewal rates in professionally managed coliving.