Project Background

Located at 469 La Trobe Street, Melbourne, the proposed project examines the adaptive reuse of an existing CBD office building initially identified in the Hassell report on Radical Re-use: From Office to Home as a candidate for office-to-residential conversion.

Since the publication of that report, the building appears to have undergone internal refurbishment. While these upgrades have improved the quality of the existing office accommodation, the asset remains fundamentally aligned to a traditional commercial use.

In a city where patterns of work have shifted and demand for well-located urban housing continues to grow, the building presents an opportunity for strategic repositioning, rather than continued investment in office-focused improvements.

A Repositioning Strategy, Not a Conventional Acquisition

This project is conceived as a strategic repositioning of an existing asset, not as a conventional acquisition-led development.

The feasibility assumes the current owner is evaluating a change of use for the building, rather than a third-party purchaser acquiring the asset at prevailing office market values and then undertaking conversion works.

This distinction matters.

If the building were acquired today at a market-clearing office valuation and subsequently repositioned into co-living, a material portion of the value uplift would be absorbed by the acquisition price. Returns would compress, and the project would present a very different risk profile.

In this scenario, value is created through structural change rather than financial leverage. A shift in use. An increase in residential density. A hospitality-led operating model applied to an already-controlled asset.

The outcomes explored later in this article should therefore be understood as situational, not generic. They reflect the efficiency of repositioning within an existing ownership structure, not a repeatable acquisition benchmark.

Reimagining the Building as a Vertical Neighbourhood

The proposed conversion reimagines the asset as a complete vertical neighbourhood. Functions once designed to serve office workers are replaced with spaces that support long-term living, wellbeing, and community.

The former parking level is repurposed as a gym. Given the building’s central location and access to public transport, a full parking level no longer reflects how residents move through the city. Instead, the gym becomes a shared wellness anchor for residents and external members, activating the building throughout the day.

Level two transitions into a coworking space accessible to both residents and non-residents. This provides practical workspace for those living in the building while generating a supplementary income stream. Levels three through sixteen are reconfigured into co-living accommodation, each supported by generous communal kitchens, dining areas, and shared living spaces designed to encourage routine and connection.

Above the existing structure, six new levels are added using lightweight CLT construction. One level is partially dedicated to shared amenities, while the remaining levels accommodate additional co-living rooms. The rooftop is transformed into an open-air communal terrace, supporting informal gatherings and strengthening the social fabric of the building.

How to Read the Financial Outcomes

Before turning to feasibility outcomes, it is important to clarify how the financial analysis should be interpreted.

The performance explored in Part Two is not presented as a development template or a repeatable acquisition strategy. It reflects a specific repositioning scenario applied to an existing asset under current ownership.

The value uplift emerges from operational and structural change rather than market arbitrage. Once acquisition pricing is reintroduced, much of that uplift is naturally absorbed. The economics shift. Returns compress. Risk reallocates.

The purpose of the analysis is not to promote headline returns, but to illustrate where value is created when asset owners begin to consider the repositioning of underperforming office buildings into co-living assets.

A Building Experienced as a Lived System

Rather than viewing the tower as a stack of disconnected floors, the building is conceived as a sequence of lived experiences.

Residents move from private rooms to shared kitchens, from communal spaces to coworking, wellness facilities, and finally the rooftop.

The building supports daily rhythms.

It provides privacy and autonomy within individual rooms.

It offers places for shared meals, focused work, exercise, and moments of social exchange.

Its economic performance emerges directly from this lived system

* Source: Radical Re-Use: From Office to Home, Hassell, 2023

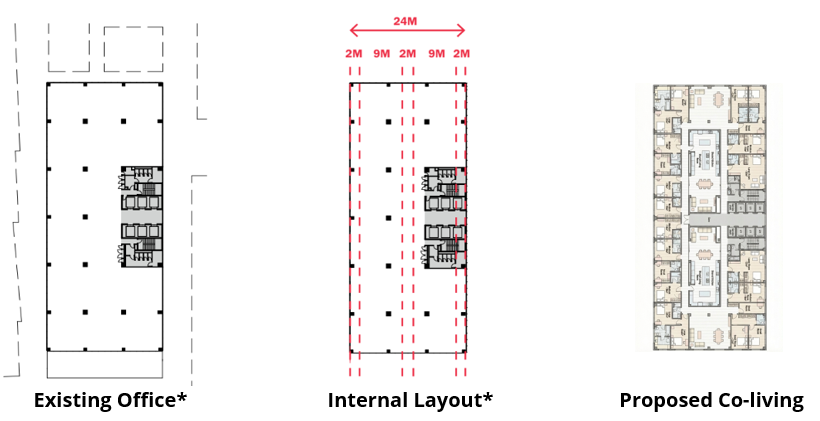

Accommodation Layout

The residential component includes a mix of small rooms of approximately 18 square metres, medium rooms of 20 square metres, and larger rooms of 25 square metres. Rooms are semi self-contained, with private bathrooms supported by shared kitchens and communal living spaces on each level.

Each floor also contains a dedicated laundry equipped with multiple machines serving residents on that level. This layout balances privacy with community. Residents retain autonomy while participating in daily shared rituals that form the social core of the building.

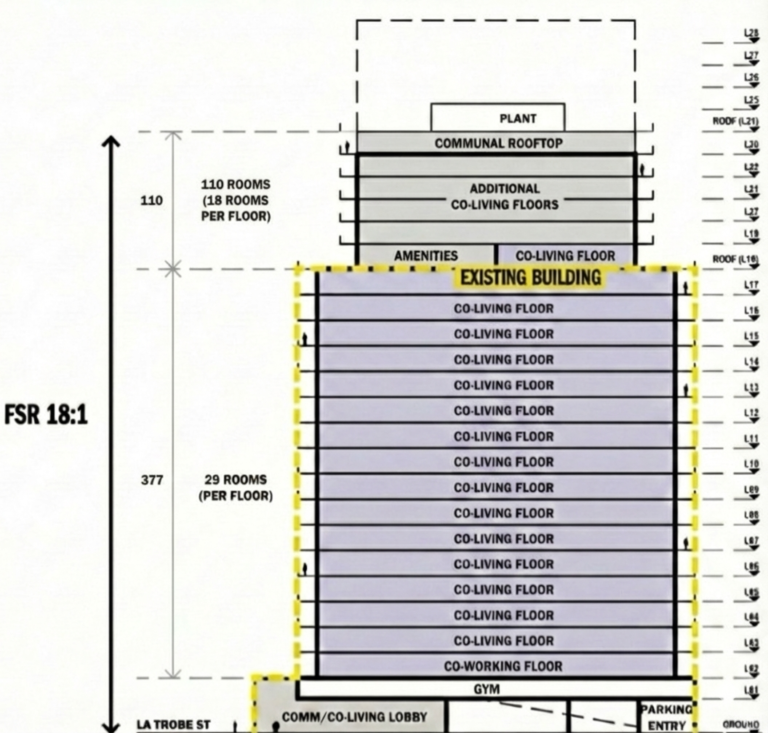

Project Overview

Total rooms:

591 co-living rooms across renovated floors and new CLT levels.

Building configuration:

Ground level: Arrival lobby

Level 1: Gym and wellness facilities (Former car park)

Level 2: Coworking for residents and external members

Levels 3-16: Co-living accommodation

Level 17: Dedicated communal floor

Level 18: Dedicated communal floor

Level 18-23: Co-living accommodation

Rooftop: Communal rooftop area

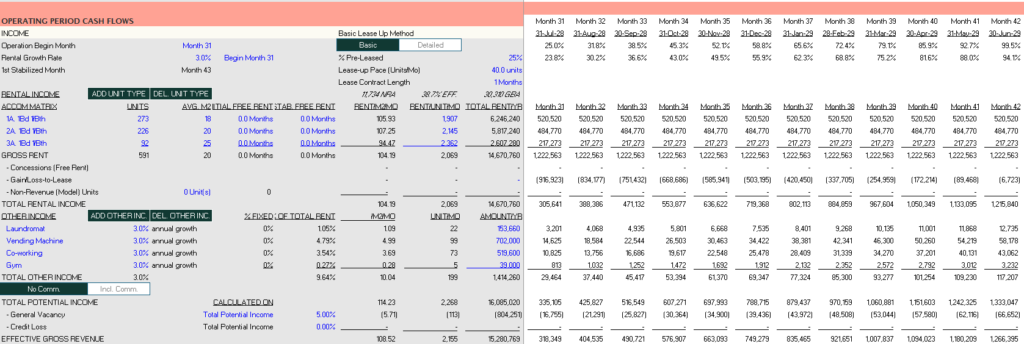

Development Timeline Assumptions

- Construction Duration: 18 months

- Pre-Leasing: 25 percent of rooms pre-leased at opening

- Lease-Up Period: 12 months

- Stabilised Occupancy: Achieved by end of Month 42

- Exit Timing: End of Year 5

These assumptions reflect the leasing behaviour typical of high-demand co-living assets in walkable CBD markets.

The Numbers Behind the Vision

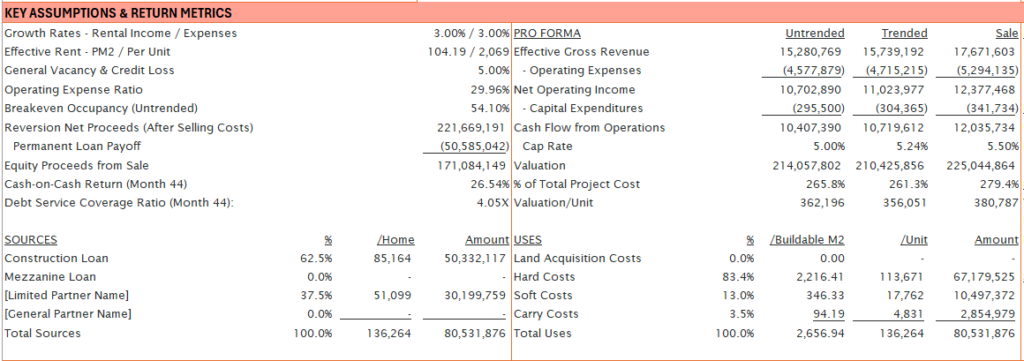

Feasibility Summary

Total Development Cost (TDC)

Approximately $80.5 million

This reflects the full cost of delivery, including construction works, soft costs, contingencies, FF&E, and capitalised interest through completion.

Capital Structure

The project is funded through a balanced mix of equity and debt designed to optimise cost of capital while maintaining strong downside protection.

Equity: 37.5%, or approximately $30.2 million

Construction debt: 62.5% at an assumed 7.0% interest rate

Permanent debt: Interest-only facility assumed at 5.40%

At stabilisation, the asset achieves a Debt Service Coverage Ratio of approximately 4.05×, providing comfortable interest coverage and long-term financing resilience.

Revenue Assumptions (Untrended)

Residential income is driven by 591 private rooms with a blended average rent of approximately $2,069 per month, equating to $14.7 million per year at full potential.

Lease-up assumptions reflect conservative absorption:

25% of rooms pre-leased at opening

Remaining rooms absorbed progressively post-completion

Stabilised occupancy of approximately 95 percent

Ongoing vacancy is assumed at 5 percent.

Diversified Ancillary Income

In addition to residential rent, the building generates supplementary income from shared amenities and services.

Coworking

Laundry

Vending machines

Gym access

Together, these streams contribute approximately $1.41 million per year, reinforcing income resilience and reducing reliance on a single revenue source.

Operating Performance

Annual operating expenses are assumed at approximately $4.6 million, inclusive of management, utilities, maintenance, insurance, and asset-level reserves.

After operating costs and capital allowances, the asset generates a stabilised Net Operating Income of approximately $10.7 million per year.

This level of performance materially exceeds conventional multifamily outcomes, driven by operational density, shared infrastructure, and high utilisation of space.

Cash Flow and Leverage Outcomes

Under the assumed permanent financing structure, annual debt service is approximately $2.7 million, resulting in post-financing cash flow of roughly $7.7 million per year at stabilisation.

This supports a cash-on-cash return of approximately 26.5%, reflecting strong income durability alongside conservative leverage.

Exit Profile and Equity Outcomes

At exit, based on a conservative terminal capitalisation assumption, the asset supports a valuation of approximately $225 million.

Over the hold period, equity investors receive:

$50.2 million in cumulative operating cash flow, and

$171.1 million in equity returned at sale, after debt repayment

This equates to approximately $221.3 million in total equity distributions.

Financial Outcome at Stabilisation

Stabilised Net Operating Income of approximately $10.7 million per year

Interest-only permanent debt supported by a Debt Service Coverage Ratio of approximately 4.05×

Annual post-financing cash flow of approximately $7.7 million

Implied value materially in excess of total development cost under conservative terminal assumptions

What This Project Demonstrates

This feasibility illustrates more than financial performance.

It shows how thoughtful design, hospitality-led operations, and a clear repositioning strategy applied within an existing ownership structure can materially change how an urban building functions over time.

Buildings are not static. They evolve in response to how people live, work, and connect.

This project serves as a reference point for how underperforming office assets, in the right ownership context, can be repositioned into viable, human-centred urban living environments.